Assignment:

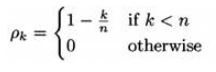

Consider a moving-average algorithm with time window n. Assume that the observed values are i.i.d. variables. Show that the autocorrelation function for two forecasts that are k time buckets apart is

Provide complete and step by step solution for the question and show calculations and use formulas.