Question 1: The Harold Shipman Private Healthcare Clinic Ltd specialises in hip, knee and shoulder replacement operations that it carries out for private health insurance firms and for some NHS Trusts. As well as providing these surgical procedures it offers pre-operative and post-operative care in a fully equipped private hospital for patients undergoing these procedures. Surgeons are paid a fixed fee for each procedure they perform and an additional amount for each follow up consultation which are given if post operative complications arise. No extra fee is charged to patients for follow up consultations. All the other staff receives annual salaries.

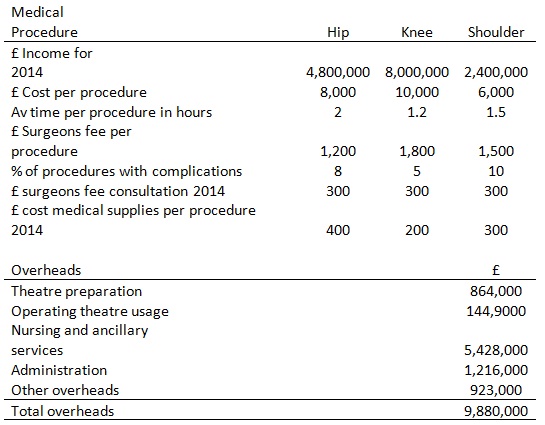

The company’s overhead is currently apportioned on revenues to each surgical specialism. The following forecast data for 2014 is made available:

Required:

i) Prepare a Marginal Cost Analysed Income Statement for 2014 from the above data to identify total and individual medical procedure contributions and profits (apportion the overheads as indicated above to each procedure). Identify the profit and contribution per procedure.

ii) The senior surgeon has voiced the opinion that apportioning overheads on the basis of revenues is misleading and instead should be apportioned on the number of hours incurred on each procedure. Reconstruct the Marginal Cost Analysed Income Statement to reflect this proposed accounting treatment. Also identify the profit and contribution per procedure. Comment on your results.

iii) The Scutari NHS Trust has approached the clinic to undertake some additional knee operations. This would involve operating on a further 50 patients which the clinic has capacity to handle. The trust is offering to pay £250,000 for fulfilling the contract. Advise the clinic what decision should be made regarding the proposed contract based on financial grounds.

Question 2: You have been appointed as a management intern in the Carbon Neutral Group Plc an international company manufacturing alternative green energy systems. This involves you obtaining a wide company experience by working in different divisions of the company. Currently you have been seconded to the production department.

At a production departmental meeting you hear Richard Head the production manager state that,

“Budgeting is a waste of time. I don’t see the point of it. It tells us what we can’t afford but it doesn’t keep us from buying it. It simply makes us invent new ways of manipulating figures. If all levels of management aren’t involved in the setting of the budget, they might as well not bother preparing one.”

Required:

In an academic essay identify and explain the objectives of a budgetary control system and discuss the concept of a participative style of budgeting in terms of the objectives you have identified supported by credible academic citations.