Where is the price elasticity of supply unitary

The price elasticity of supply as in below demonstrated figure is unitary within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Hey friends please give your opinion for the problem of Economic that is given above.

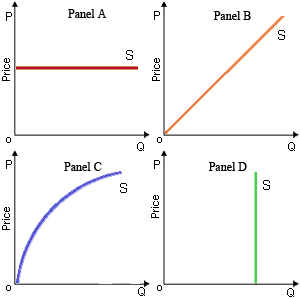

The price elasticity of supply as in below demonstrated figure is unitary within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D.

Hey friends please give your opinion for the problem of Economic that is given above.

The supply curve most consistent along with the inelastic supply of land into Antarctica is demonstrated in: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Q : Economic profit generating purely In this illustrated figure in below the only purely competitive firm currently generating economic profit is in: (w) Firm A. (x) Firm B. (y) Firm C. (z) Firm D. Q : Problem on financial Intermediation The The main reason for the existence of financial intermediaries is as: (1) Direct flows of savings from the individuals to firms would necessitate higher transaction costs. (2) That just wealthy individuals can afford to invest in the stocks and bonds. (3) The habits of

In this illustrated figure in below the only purely competitive firm currently generating economic profit is in: (w) Firm A. (x) Firm B. (y) Firm C. (z) Firm D. Q : Problem on financial Intermediation The The main reason for the existence of financial intermediaries is as: (1) Direct flows of savings from the individuals to firms would necessitate higher transaction costs. (2) That just wealthy individuals can afford to invest in the stocks and bonds. (3) The habits of

The main reason for the existence of financial intermediaries is as: (1) Direct flows of savings from the individuals to firms would necessitate higher transaction costs. (2) That just wealthy individuals can afford to invest in the stocks and bonds. (3) The habits of

Whenever the market for the good is in equilibrium, this signifies that the: (i) Demand and supply are equivalent. (ii) Tax wedge is perfectly offset by the government advantages. (iii) Differences among demand prices and supply prices equivalent profit per unit. (iv)

Can someone help me in finding out the right answer from the given options. The employer who amplifies the safety of a place or prospects for advancement to the job applicants makes inefficiencies (or arguable inequities) since of: (1) Signaling. (2) Credentialism. (3

Select the right ans wer of the question. Which of the following would we expect to contain the highest poverty rate? A) white households headed by males B) elderly white households C) white households headed by females D) African-American households headed by femal

When a monopolist raises price, it: (w) always increases its revenue. (x) always reduces its revenues. (y) doesn't influence its revenue. (z) may increase, decrease, or not change total revenue. I need a good answe

Describe the Law of Diminishing marginal utility? Answer: Law of Diminishing marginal utility: As a consumer goes on consuming more and more units of a commodity th

When an incumbent firm uses an edge pricing strategy: (w) this can maximize short run profits and discourage entry in the market. (x) this may not be maximizing short run profits, but this can make positive economic profits over the long run. (y) the

Purely competitive industries operating under circumstances of constant cost have long-run supply curves which are: (w) horizontal. (x) upward sloping. (y) downward sloping. (z) equal to LRATC for every firm. Can a

18,76,764

1933611 Asked

3,689

Active Tutors

1415553

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!