Where is demand perfectly price inelastic at price

For Pixie's cheesy fried grits demand is perfectly price inelastic at a price of: (w) P4. (x) P2. (y) 0. (z) None of the above. Please choose the right answer from above...I want your suggestion for the same.

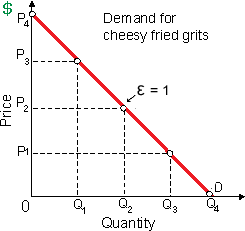

For Pixie's cheesy fried grits demand is perfectly price inelastic at a price of: (w) P4. (x) P2. (y) 0. (z) None of the above.

Please choose the right answer from above...I want your suggestion for the same.

Elucidate briefly business cycles and what role do the Federal Government and Federal Reserve has in trying to manage them?

One of my friends can't succeed to get the solution of this question. Give me solution of this question. Under what circumstances can monopolistic competition and oligopoly describe stable prices?

Short-run supply curve of a purely competitive firm is the positively sloped segment of: (a) its long run sales revenue curve. (b) its marginal fixed cost curve. (c) its average profits curve. (d) its average total cost curve. (e) its MC curve above t

For Cournot’s Spring Water the demand is perfectly price elastic at: (i) point a. (ii) point b. (iii) point c (iv) point d. (v) point e. Q : Oligopoly output control by An industry dominated by some consciously interdependent firms which control most of its output is an: (1) uncontestable market. (2) oligopoly. (3) illegal conspiracy. (4) unnatural monopoly. (5) entrepreneurial cartel. Can someone

An industry dominated by some consciously interdependent firms which control most of its output is an: (1) uncontestable market. (2) oligopoly. (3) illegal conspiracy. (4) unnatural monopoly. (5) entrepreneurial cartel. Can someone

A uniform resource price paid for any resource which has an aggregate supply curve which is less than perfectly elastic generates an: (1) exploitation ratio. (2) investment surcharge. (3) accounting profit. (4) economic rent. (5) acce

Normal 0 false false

Purely competitive markets share the feature of: (i) collusive behavior among of large firms. (ii) freedom of entry and exit in the long run. (iii) extensive negotiations about prices in between buyers and sellers. (iv) widespread product differentiat

Assume that many students have fixed “pizza budgets.” When the price per slice falls by $10 to $1 along such demand curve for pizza weekly near a college campus, then the price elasticity of demand for pizza: (w) rises towards infinity. (x

For a negative income tax the break-even level of income plan (NIT) is: (1) negatively related to the plan’s basic income floor. (2) positively related to the negative income tax rate. (3) a main influence on the total cost of t

18,76,764

1924490 Asked

3,689

Active Tutors

1442851

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!