When is demand perfectly price inelastic

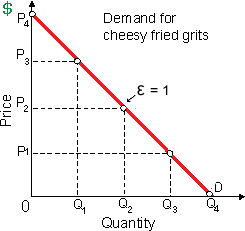

Demand is perfectly price inelastic when the quantity demanded for Pixie’s cheesy fried grits is of: (w) zero. (x) P4. (y) P2. (z) More information is required. How can I solve my Economics problem? Please suggest me the correct answer.

Demand is perfectly price inelastic when the quantity demanded for Pixie’s cheesy fried grits is of: (w) zero. (x) P4. (y) P2. (z) More information is required.

How can I solve my Economics problem? Please suggest me the correct answer.

I have a problem in economics on Market Supplies of Labor. Please help me in the following question. In long run, the labor supply curve facing the major industry: (i) Will always be positively associated to the wage rate. (ii) Will slope upward if and only if individ

Outputs and average prices for CDs and DVDs both rose throughout 1999 to 2000 (just before file sharing became ordinary), implying such that: (1) supply of prerecorded music should have grown. (2) law of demand does not apply to music. (3) demand for

assume the firm is a price taker and faces a market price of €60 per unit. draw the AR and MR curves

A firm can practice price discrimination to increase its profitability when this: (w) confronts a perfectly elastic demand curve. (x) is a pure quantity adjuster. (y) has some market power and is able to separate its customers into various groups alon

When the distributions of income were suitable, when there were no externalities, and when the economy was purely competitive, in that case market forces would yield production and distribution of penicillin consequent to: (i) point a. (ii) point b. (

When resource markets are competitive and transaction costs are low, in that case landowners: (1) pass forward completely any land tax. (2) can drive up the rental rate of land by changing its supply. (3) bear the full burden of any t

As comparing income and wealth: (w) differences in their distributions reflect economic discrimination precisely. (x) wealth is a flow variable, whereas income is a stock variable. (y) inheritance explains income differences more totally than wealth d

When the price Pixie’s Restaurant charges for its well-known cheesy fried grits rises from $2 to $4 and quantity demanded falls from 750 to 500 servings weekly, the price elasticity of demand over such price range is approximate

For a gain maximizing competitive firm operating in the competitive labor market, the: (1) Marginal resource cost of the labor is similar to the wage rate. (2) Supply of the labor is perfectly inelastic. (3) Production quota is precisely proportional to the labor hire

As MRP < VMP in imperfect competition whenever firms encompass market power as sellers then: (1) MPPL = VMP. (2) The price of output surpasses MFC. (3) Monopolistic exploitation becomes essential to get profit. (4) Imperfect competition can’t reach the equili

18,76,764

1937488 Asked

3,689

Active Tutors

1459159

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!