Wage rate and labor in supplying

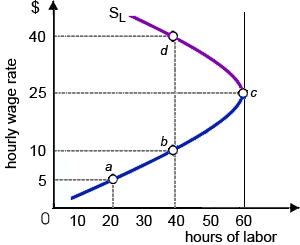

By the following choices in this illustrated graph, this worker would be happiest at point: (w) point a. (x) point b. (y) point c. (z) point d. Please choose the right answer from above...I want your suggestion for the same.

By the following choices in this illustrated graph, this worker would be happiest at point: (w) point a. (x) point b. (y) point c. (z) point d.

Please choose the right answer from above...I want your suggestion for the same.

challenges of Equilibrium picing in devloping countries

Explain the term average fixed cost.

What are the external factors in governing prices?

If a perfectly competitive firm determines that its market price is below its minimum average variable cost, this will sell: w) the output where marginal revenue equivalents marginal cost. x) any positive output the entrepreneur decid

Illustrates the Income Elasticity of Demand?

Give a brief introduction of the term Break Even Point. How does BEP aid in making business decision?

Extra revenue by the extra output produced from an additional unit of a resource is the marginal resource: (1) profit to the firm. (2) revenue product. (3) iso-utility curve. (4) resource cost. (5) productive value. Q : What is Diminishing Returns to Scale What is Diminishing Returns to Scale?

What is Diminishing Returns to Scale?

dear Please read carefully about in structure and requirement of the assessment. I need quality work with academic writing with less than 5% similaraies and make sure if any studens ask same assessment to avoid plagiarism

Workers who keep their jobs will be more productive after firms adjust to raises in: (1) competition in an industry. (2) wages. (3) technological advances. (4) capital costs. (5) government regulation. Hey friends please give your

18,76,764

1954495 Asked

3,689

Active Tutors

1419467

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!