Variation in price elasticity as price of output

The only supply curve which has price elasticity which varies as the price of output increases is within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Hello guys I want your advice. Please recommend some views for above Economics problems.

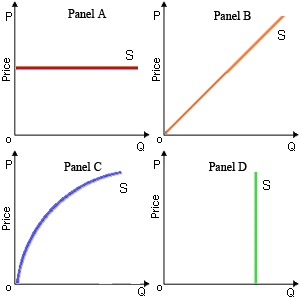

The only supply curve which has price elasticity which varies as the price of output increases is within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D.

Hello guys I want your advice. Please recommend some views for above Economics problems.

Conditions of producers equilibrium: The conditions of producers equilibrium through the marginal cost and marginal revenue approach are as follows. 1. Marginal cost should be equal to marginal revenue.

How is TVC derived from MC? Answer: TVC = Sigma MC

Lowering prices will raise total revenue from DVD game sales at all prices as: (w) on this demand curve. (x) below $25. (y) above $25. (z) below $30. Q : Define investment demand function Investment demand function: Investment demand function is the relationship among rate of interest and investment demand. There is an inverse relationship among the rate of interest and investment demand. High inter

Investment demand function: Investment demand function is the relationship among rate of interest and investment demand. There is an inverse relationship among the rate of interest and investment demand. High inter

Can someone please help me in finding out the accurate answer from the following question. The United Auto Workers (or UAW) is an illustration of the: (1) Industrial union. (2) Company union. (3) Mechanical union. (4) Craft union.

Breaking a natural monopoly within a number of competing firms would probably: (w) increase output and lower price to consumers. (x) reduce output and raise price to consumers. (y) reduce efficiency but lower price. (z) have no effect on output or pri

From about 1890 till 1970 year, the “structure-conduct-performance paradigm” dominated theories regarding how firms behave in various types of markets. The term here “performance” in this context refers to those things as: (i)

When the equality standard of income distribution were adopted: (w) people would be paid the values of their marginal products. (x) family incomes would be identical for families of all sizes. (y) poets and engineers would have the same incomes. (z) g

The income stream per period like a percentage of the dollar outlay for investment into a capital good is the: (1) present value of the investment good. (2) rate of economic profit. (3) interest rate. (4) rate of retu

Question: (1) Suppose the jeans industry is an oligopoly in which each firm sells its own distinctive brand of jeans, and each firm believes its rivals will not follow its price increases but will

18,76,764

1935065 Asked

3,689

Active Tutors

1444722

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!