Variation in demand curve with price elasticity

The demand curve along with price elasticity which definitely varies along the curve is within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Can anybody suggest me the proper explanation for given problem regarding Economics generally?

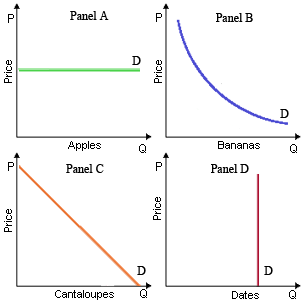

The demand curve along with price elasticity which definitely varies along the curve is within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?

The theory of monopolistic competition was developed through: (1) Alfred Marshall. (2) John Maynard Keynes. (3) Joseph Schumpeter. (4) Edward Chamberlin. (5) Antoine Augustin Cournot. Please choose the right answer

Describe the implication of perfect knowledge regarding market beneath perfect competition.

The government price floor for Whopper Slushees at P3 would result a: (i) shortage of Q1 – Q3. (ii) Excess of Q3 - Q1. (iii) Supply price of P1. (iv) Quantity demanded of Q2. (v) Demand price of P2. Q : In the quintile distribution of income In the quintile distribution of income, the term "quintile" represents

In the quintile distribution of income, the term "quintile" represents

Monopolistic competitors: (1) base decisions on the anticipated reactions of their many individual competitors. (2) can easily enter but not exit industries. (3) may sometimes act like monopolists and gain economic profits in the short run because of

The proposition which taxing the rich to provide to the poor improves social welfare can’t be proved due to the impossibility of: (1) developing a political consensus about efficient redistribution programs. (2) the marginal utility of income di

Objectives: This assessment item relates to the course learning outcomes 1, 2 and 3 as listed in Part A. Question 1 (22 marks) (a) Consider the market represented by the schedule in the table below. (5 marks) Price Quantity demanded Quantity

Within a monopolistically competitive industry along with no barriers to entry, long run equilibrium will be reached along with the firms into the industry: (1) maximizing total revenue. (2) producing their most efficient outputs. (3)

The resource which a carpet manufacturer is most probable to view as the variable in short run would be: (i) The warehouse it owns (ii) Truck driver. (iii) The truck on a 5-year lease agreement. (iv) Firm’s biggest factory. C

Why does a good or service become a public good or service?

18,76,764

1955107 Asked

3,689

Active Tutors

1435578

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!