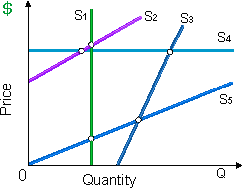

Supply is unitarily price elastic for all quantities and prices upon: (i) supply curve S1. (ii) supply curve S2. (iii) supply curve S3. (iv) supply curve S4. (v) supply curve S5.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.