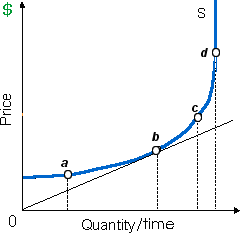

At point b, in demonstrated figure the supply curve into this graph is: (w) perfectly elastic. (x) elastic, but not perfectly that why. (y) unitarily elastic. (z) inelastic.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?