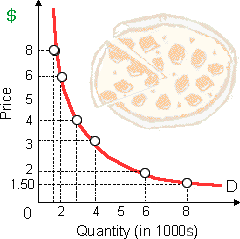

On such demand curve for pizza as in below demonstrated graph, there demand is: (w) elastic for all prices and quantities demonstrated. (x) unitarily elastic for all prices and quantities shown. (y) elastic at high prices and inelastic at low prices. (z) inelastic at all prices and quantities demonstrated.

Hey friends please give your opinion for the problem of Economic that is given above.