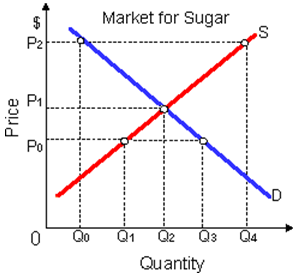

These supply and demand curves within the sugar market specify that: (w) a price floor of P0 for sugar will cause a surplus. (x) a price ceiling of P2 will cause a shortage. (y) the market clears while quantity equals Q0. (z) at P2, unexpected inventory development will push price towards P0.

Hello guys I want your advice. Please recommend some views for above economics problems.