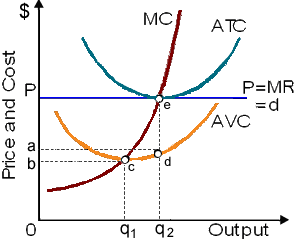

When this firm is a typical pure competitor within this industry as in demonstrated figure, then the firm is: (i) making normal accounting profit. (ii) making zero economic profit. (iii) breaking even. (iv) into an industry within long run equilibrium. (v) All of the above.

How can I solve my Economics problem? Please suggest me the correct answer.