Total variable cost while maximizes economic profits

Total cost when such firm maximizes economic profits would be: (w) $72,000 per period. (x) $80,000 per period. (y) $96,000 per period. (z) $100,000 per period. Hello guys I want your advice. Please recommend some views for above Economics problems.

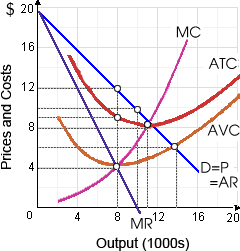

Total cost when such firm maximizes economic profits would be: (w) $72,000 per period. (x) $80,000 per period. (y) $96,000 per period. (z) $100,000 per period.

Hello guys I want your advice. Please recommend some views for above Economics problems.

Most historical studies intended to categorize and quantify poverty within the United States: (w) consider both assets as well as money income. (x) conclude which almost one-half of all families are below the poverty level. (y) suggest that from the 1

A characteristic Hollywood star derives the maximum consumer surplus from: (i) Calvin Klein underwear. (ii) Water. (iii) Mercedes Benz 600SEs. (iv) DeBeers diamonds. (v) Publicity in "The National Enquirer." Can so

please find the attached file (project) and qoute for it. minimus 7 pages required.

Economic rent by a parcel of land is positively associated to the: (w) savings in transaction costs yielded by its location. (x) amount of idle land adjacent to this. (y) time this has been held by the current landowner. (z) amount of natural flora an

Marginal revenue is not below the market price by the perspectives of simply: (i) monopolistic competitors. (ii) monopolists. (iii) cartel members. (iv) pure oligopolists. (v) pure competitors. Can

Can someone help me in finding out the right answer from the given options. The employer who amplifies the safety of a place or prospects for advancement to the job applicants makes inefficiencies (or arguable inequities) since of: (1) Signaling. (2) Credentialism. (3

The quantity supplied is ever more sensitive as output increases, therefore the price elasticity of supply raises as the price raises for the supply curve demonstrated in: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D.

When the quantity of SCUBA lessons demanded by Hawaiian tourist’s increases from 800 to 1,000 weekly and if the price drops/falls from $30 to $20 per session, by using the arc elasticity formula, the price elasticity of demand will be: (i) 5.555

Select the right ans wer of the question.Nonrivalry and nonexcludability are the main characteristics of: A) capital goods. B) private goods. C) public goods. D) consumption goods.

The demand curve facing a monopolistically competitive firm might shift rightward when this: (w) increases wages to workers. (x) experiences a decline in costs. (y) advertises successfully. (z) responds strategically to competitors&rs

18,76,764

1923069 Asked

3,689

Active Tutors

1446412

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!