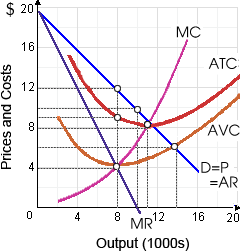

Total variable cost when this firm maximizes economic profits would be: (i) $12,000 per period. (ii) $24,000 per period. (iii) $32,000 per period. (iv) $48,000 per period. (v) $60,000 per period.

Hey friends please give your opinion for the problem of Economics that is given above.