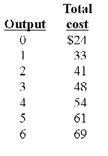

Total variable cost

By refering the following data give the answer of this question . The total variable cost of producing 5 units is: A) $61. B) $48. C) $37. D) $24.

A monopoly is a type of market structure in that one: (w) seller produces whole industry’s output. (x) giant firm is a price taker. (y) barrier to entry exists. (z) giant firm is the single buyer of resources. Q : Elasticity and Revenue At the point of At the point of unit elasticity beside the demand curve then a firm faces: (w) profits are always maximized. (x) total revenue is certainly at a maximum. (y) total costs are minimized. (z) All of the above. I need

At the point of unit elasticity beside the demand curve then a firm faces: (w) profits are always maximized. (x) total revenue is certainly at a maximum. (y) total costs are minimized. (z) All of the above. I need

The Department of the Census explains low relative income as experienced while families: (w) lack sufficient income to buy the fundamental food clothing and shelter required for survival. (x) would like to improve the

When the wholesale price per bushel of peaches is $9, Cling Peach Orchards would be probably to break even when its peach orchard produced approximately: (i) 2000 bushels of peaches. (ii) 2500 bushels of peaches. (iii) 3000 bushels of

The demands for vast new sport utility vehicles [or SUVs] like Hummers and Ford Explorers would most likely reduce most sharply in response to a 50%: (i) Rise in the annual cost of driver’s license. (ii) Decreasing in rent on luxury apartments on the center of b

At the point upon the demand curve for Silver Screen Classic DVDs, here the price elasticity of demand is unitary, the price would be approximately: (i) $10, resulting in roughly 8 million DVDs being sold. (ii) $13, resulting in appro

The interest rate ____ as well as the present value of future income ____ when the preference for current income over the future income weakens. (w) falls; rises. (x) rises; falls. (y) falls; falls. (z) rises; rises. Q : Managerial slack or X-inefficiency X-inefficiency (also termed as managerial slack): (1) tends to drive up fixed costs. (2) commonly results from firms not being hard pressed through competitors. (3) can absorb much of a monopoly’s potential profit. (4) is a prob

X-inefficiency (also termed as managerial slack): (1) tends to drive up fixed costs. (2) commonly results from firms not being hard pressed through competitors. (3) can absorb much of a monopoly’s potential profit. (4) is a prob

Which of the given in lists of taxes or taxed goods is possibly in accurate order from most backward-shifted to most forward: (w) Tobacco, property, general sales and payroll. (x) Land, payroll, tobacco and property. (y) Tobacco, payroll, corporate in

The demand curve facing an unregulated non-discriminating monopolist is NOT: (w) similar as the industry's demand curve. (x) downward sloping. (y) more elastic than the demand curve facing a competitive firm. (z) various from its marg

18,76,764

1951753 Asked

3,689

Active Tutors

1424833

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!