Total revenue for profit-maximizing pure competitor

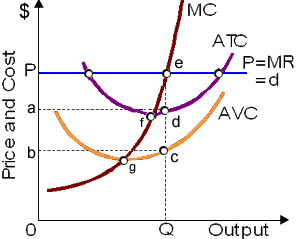

TR (total revenue) for this profit-maximizing pure competitor equivalents area: (i) 0PeQ. (ii) bPec. (iii) aPed. (iv) 0bcQ. (v) 0Pec. Can someone explain/help me with best solution about problem of Economics...

TR (total revenue) for this profit-maximizing pure competitor equivalents area: (i) 0PeQ. (ii) bPec. (iii) aPed. (iv) 0bcQ. (v) 0Pec.

Can someone explain/help me with best solution about problem of Economics...

Can someone please help me in finding out the accurate answer from the following question. The monopsonist will hire the labor until labor's marginal resource cost equivalents the: (i) Marginal revenue product of the labor. (ii) Marginal physical product. (iii) Value

Within the long run a monopolistically competitive firm will not be characterized through: (w) zero economic profit. (x) price greater than marginal revenue. (y) production at lowest possible average total cost. (z) price greater than marginal cost.

Refer to the budget line illustrated in the diagram given. If the consumer's money income is $20, the: 1) prices of C and D cannot be determined.2) price of C is $2 and the price of D is $4. 3) consumer can obtain a combination of 5 units of both C and D. 4)

I have a problem in economics on Price takers in product market. Please help me in the following question. Relative to firms which are price takers in product market, and then firms with market power tend to. (1) Hire some workers (2) Pay a lower wage

Elucidate the central problems of an economy: A) What to produce? B) How to produce? C) For whom to produce? Answer: Q : Marginal revenue in selling extra unit The price a firm acquires from selling an extra unit of output, minus any revenue lost when price should be reduced in all other units sold, equals: (1) average revenue. (2) marginal profit. (3) mark-up price. (4) marginal revenue. (5) total revenue.<

The price a firm acquires from selling an extra unit of output, minus any revenue lost when price should be reduced in all other units sold, equals: (1) average revenue. (2) marginal profit. (3) mark-up price. (4) marginal revenue. (5) total revenue.<

The employees at times pose principal-agent problems for the firm’s owners in the deficiency of constant monitoring. Such problems are most probable to be lessened when a firm adopts the policy of: (1) dynamically opposing the attempts to unionize. (2) Paying em

Exit from a competitive industry will carry on till economic: (w) losses are driven to zero. (x) profits precisely offset accounting losses. (y) profit exceeds accounting profit. (z) resources have minimum incomes.

The knowledge regarding local trees and shrubs which Morgan learns as working as an apprentice landscaper in suburbs of a big city is an illustration of the advantages from: (i) Dirty work. (ii) Dues-paying. (iii) General training. (iv) High-skilled employment. (v) Sp

The "kinked-demand-curve" model was developed into the 1930 year in part to help describe: (i) barriers to entry in oligopoly markets. (ii) the allegedly excessive stickiness of prices into oligopolistic industries. (iii) how competitive industries be

18,76,764

1925373 Asked

3,689

Active Tutors

1453454

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!