Total revenue for profit-maximizing

TR stands for total revenue for this profit-maximizing pure competitor as in below figure equals area: (i) 0Phq2. (ii) 0bgq2. (iii) Pbgh. (iv) 0aeq1. (v) daef. Hello guys I want your advice. Please recommend some views for above Economics problems.

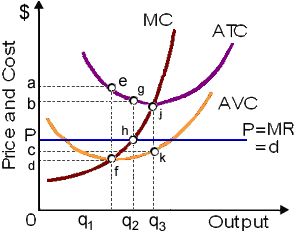

TR stands for total revenue for this profit-maximizing pure competitor as in below figure equals area: (i) 0Phq2. (ii) 0bgq2. (iii) Pbgh. (iv) 0aeq1. (v) daef.

Hello guys I want your advice. Please recommend some views for above Economics problems.

When this firm initially had important market power along with potential long-run economic profit, a likely cause of the firm finally being in a stable equilibrium of an $18 price and output of 5,000 units every day would be: (1

An increase in consumer desire for strawberries is most likely to: increase the number of strawberry pickers needed by farmers. reduce the supply of strawberries. reduce the number of people willing to pick strawberries. reduce the need for strawberry pickers

Refer to the given figure.Choose the right answer from following. If the relevant saving schedule were constructed: A) saving would be minus $20 billion at the zero level of income. B) aggregate saving would be $60 at the $60 billion level of income. C) its slope woul

When all households have equal incomes, in that case the Lorenz curve would be: (w) zero. (x) a 45 degree line. (y) 1. (z) rectangularly hyperbolic. Hey friends please give your opinion for the problem of E

The amount of goods which people are willing and capable to buy is termed as their: (i) Desires. (ii) Demands. (iii) Requirements. (iv) Needs. (v) Wants. Can someone please help me in finding out the accurate answe

Barriers to entry which may protect monopolistic firms through losing market power across time do not comprise: (i) legal or regulatory barriers. (ii) artificial barriers. (iii) collusive barriers. (iv) strategic barriers. (v) natural

Can someone please help me in finding out the accurate answer from the following question. Declines in international price of oil would be most probable to cause: (1) Wages of bicycle factory workers to rise. (2) Demand for automobiles to reduce. (3) Incomes of the ge

The price elasticity of supply in given grph is infinite therefore supply is perfectly price elastic within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Q : Perfect complements of Complementary I have a problem in economics on Perfect complements of Complementary Goods. Please help me in the following question. Left and right shoes are illustrations of nearly: (1) Production complements. (2) Perfect complements. (3) Joint production. (4) Per

I have a problem in economics on Perfect complements of Complementary Goods. Please help me in the following question. Left and right shoes are illustrations of nearly: (1) Production complements. (2) Perfect complements. (3) Joint production. (4) Per

When this firm is typical in this purely competitive market, in that case long-run equilibrium for Christmas trees will be reached at a market price is of: (1) P1. (2) P2. (3) P3. (4)

18,76,764

1932711 Asked

3,689

Active Tutors

1422681

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!