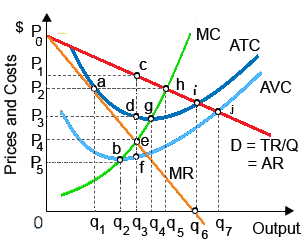

HoloIMAGine has patented a holographic technology which makes 3-D photography obtainable to consumers. The level of sales and production at that HoloIMAGine would take in its greatest probable total revenue is: (i) output q3. (ii) output q4. (iii) output q5. (iv) output q6. (v) output q7.

Hey friends please give your opinion for the problem of Economics that is given above.