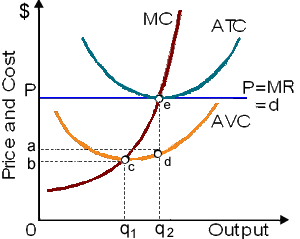

Total revenue for the firm in illustrated figure is __________ __________ total cost.: (w) greater than (x) less than (y) equal to (z) Cannot be determined by the information given.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?