Total fixed costs of purely competitive firm

Such lumber mill has incurred total fixed costs which average approximately: (1) $300 daily. (2) $500 per day. (3) $700 Per day. (4) $900 per day (5) $1100 per day. Please choose the right answer from above...I want your suggestion for the same.

Such lumber mill has incurred total fixed costs which average approximately: (1) $300 daily. (2) $500 per day. (3) $700 Per day. (4) $900 per day (5) $1100 per day.

Please choose the right answer from above...I want your suggestion for the same.

The present value of an annual income stream which goes onto forever is: (w) infinite. (x) zero. (y) the annual income multiplied through the interest rate. (z) the annual income divided through the interest rate.

Let consider the law of demand. The idea that the higher price for a normal good will outcome in less of good being purchased never based logically on the: (1) Income effect, by which the higher price decreases the purchasing power of the income. (2) Demand for good f

Can someone help me in finding out the most precise answer from the given options. The Monetary revenue produced by the firm throughout a specific period minus its explicit costs gives up: (1) Value added. (2) Gross cash flow. (3) Tax liability. (4) Economic income. (

Why borrowing is treated as capital receipts? Answer: Because it rises the liability of government.

The market supply curve is derived via: (i) Evaluating the net costs for each potential level of output. (ii) Inverting (or taking the mirror image of) the market demand curve. (iii) Horizontally summing up individual supply curves. (iv) Averaging the

One who buys gold into London and after that sells that instantly in Boston for a higher price is: (1) monopolist. (2) capitalist. (3) speculator. (4) auctioneer. (5) arbitrageur. Can anybody suggest me the proper explanation for g

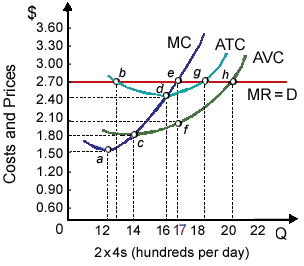

When price discrimination is not possible this profit-maximizing monopolistic competitor charges a price of $______ as well as produces ___________ units of output: (w) $12 || 5 thousand. (x) $15 || 8 thousand. (y) $16 || 7 thousand.

A firm within an imperfectly competitive market is: (w) more likely to advertise than a purely competitive firm. (x) less probable to advertise than a purely competitive firm. (y) neither more nor less probable to advertise than a pure competitor. (z)

When a monopolist reaches equilibrium: (1) its profits are at a maximum. (2) price equals marginal cost. (3) average cost is at its minimum. (4) marginal cost is at a minimum. Can someone explain/help me with best solution about pr

Marginal revenue: This refers to the addition prepared to the total revenue.

18,76,764

1960637 Asked

3,689

Active Tutors

1453042

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!