Total fixed cost in competitive firm

This competitive firm's fixed cost or TFC in demonstrated can be computed as area as: (i) 0P3fq4. (ii) P2P1de. (iii) P3P2ef. (iv) 0P2eq4. (v) aced. Hey friends please give your opinion for the problem of Economics that is given above.

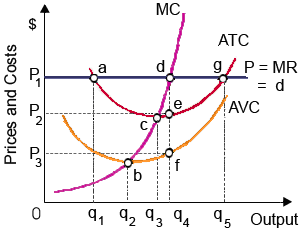

This competitive firm's fixed cost or TFC in demonstrated can be computed as area as: (i) 0P3fq4. (ii) P2P1de. (iii) P3P2ef. (iv) 0P2eq4. (v) aced.

Hey friends please give your opinion for the problem of Economics that is given above.

Elucidate GNI per capita?

The corporation’s stockholders are not personally liable for the debts of firm since: (1) The Corporation is considered as a legal person, separate from its owner. (2) Usually there are too many stockholders to try to hold them all accountable. (3) In a corporat

Can someone help me in finding out the right answer from the given options. Suppose that everything except the variables we are studying remains constant or steady is termed as the: (1) Ceteris paribus assumption. (2) Ex-ante assumption. (3) Ex-post assumption. (4) Po

Oligopolists enter within formal or informal arrangements to fix prices within attempts to: (1) stabilize prices to customers. (2) compete more effectively along with foreign competitors. (3) reduce the price elasticity of market demand. (4) max

The value of land is attributable to the ways exactly sites decrease transportation and other transaction costs are termed as: (1) location rents. (2) transportation rents. (3) short term quasi rents. (4) parcel posts. (5) transaction

Moving from point d to point e beside demand curve D, the price elasticity of demands of DVDs of video games at equal: (a) 0.8. (b) one. (c) 1.10. (d) 1.25. (e) 2.50 Q : Reflecting normal substitution by When consumer demand for this industry’s product is relatively inelastic, in that case the curve reflecting normal substitution although the least price elasticity of market demand would be of: (i) curve A. (ii) curve B. (iii) curve C. (iv) curv

When consumer demand for this industry’s product is relatively inelastic, in that case the curve reflecting normal substitution although the least price elasticity of market demand would be of: (i) curve A. (ii) curve B. (iii) curve C. (iv) curv

When the demand for Tantalizingly Tart Tangerine-ade of Tasty Toni is relatively price elastic, then Toni can boost her total revenue through: (w) raising her price. (x) keeping her price similar. (y) lowering her pri

The yellow dog contracts are now proscribed, however in the early 20th century such agreements among employers: (i) Not to purchase intermediate goods made by unionized labor hindered labor market transformations. (ii) And workers stating that the workers would not jo

When point e corresponds to $9 per copy for Silver Screen DVDs, Nostalgia Corporation can produce annual economic profit of at mostly about: (i) $25 million. (ii) $35 million. (iii) $50 million. (iv) $75 million. (v) $100 million. Discover Q & A Leading Solution Library Avail More Than 1416758 Solved problems, classrooms assignments, textbook's solutions, for quick Downloads No hassle, Instant Access Start Discovering 18,76,764 1929357 Asked 3,689 Active Tutors 1416758 Questions Answered Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!! Submit Assignment

18,76,764

1929357 Asked

3,689

Active Tutors

1416758

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!