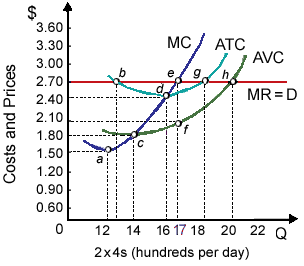

Total costs of profit-maximizing lumber mill

This profit-maximizing lumber mill incurs total costs of approximately: (a) $2200 per day. (b) $3300 per day. (c) $4200 per day. (d) $5200 per day (e) $6200 per day. How can I solve my Economics problem? Please suggest me the correct answer.

This profit-maximizing lumber mill incurs total costs of approximately: (a) $2200 per day. (b) $3300 per day. (c) $4200 per day. (d) $5200 per day (e) $6200 per day.

How can I solve my Economics problem? Please suggest me the correct answer.

Pure competition and monopolistic competition are: (1) polar opposites on the continuum of market structures. (2) the two market structures in that firms are pure quantity adjusters. (3) both characterized by an absence of barriers to long run entry a

Line T1 depicts in given graph as in below a tax system which is: (i) progressive. (ii) recessive. (iii) proportional. (iv) biased. (v) regressive. Q : Describe inferior goods in economics Inferior goods in economics: Inferior goods refer to such goods whose demand reduces with the rise in income of consumer.

Inferior goods in economics: Inferior goods refer to such goods whose demand reduces with the rise in income of consumer.

Total revenue of a pure competitor is its quantity sold that is multiplied by its: (w) profit per unit. (x) price per unit. (y) average variable cost. (z) overhead cost per unit. Can someone explain/help me with be

Multiplier: It is the number by which change in investment should be multiple in order to find out the resultant change in income and output.

The revenue added through selling an additional unit of output is: (w) demand elasticity. (x) average profit rate. (y) supply elasticity. (z) marginal revenue. How can I solve my Economics problem?

Short-run supply curve of a purely competitive firm’s is: (w) its MC curve above the minimum of the AVC curve. (x) the upward sloping part of its ATC curve. (y) the intersection where is MR = MC. (z) horizontal up to the firm’s productive

When a purely competitive industry is within equilibrium as well as all firms in the industry are operating along with economies of scale, in that case the industry is in: (w) long-run and short-run equilibrium. (x) short-run equilibrium and long run

The following is a case problem around which the examination paper will be based. In preparation for the examination, you should study the problem scenario and identify the possible public international law issues which might arise, and how the law might be applied to

Demand is perfectly price elastic when the price for Pixie's cheesy fried grits is a mostly unmeasurably small bit below the: (1) zero. (2) P1. (3) P2. (4) P3. (5) P4. Discover Q & A Leading Solution Library Avail More Than 1454224 Solved problems, classrooms assignments, textbook's solutions, for quick Downloads No hassle, Instant Access Start Discovering 18,76,764 1946386 Asked 3,689 Active Tutors 1454224 Questions Answered Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!! Submit Assignment

18,76,764

1946386 Asked

3,689

Active Tutors

1454224

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!