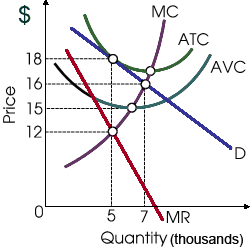

If this firm maximizes its profit as in given graph, then its total costs equal: (w) $75,000 per month. (x) $90,000 per month. (y) $15,000 per month. (z) $105,000 per month.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?