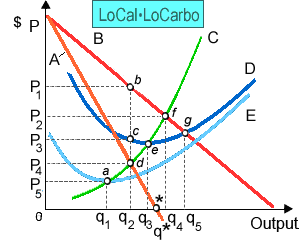

When LoCalLoCarbo produces the profit-maximizing quantity and charges the profit-maximizing price, in that case its total costs equal the area of the rectangle as: (i) 0P3cq2. (ii) bdP4P1. (iii) 0P4dq2. (iv) bcP3P1. (v) 0P2fq4.

Please guys help to solve this problem of Economics with some explanation.