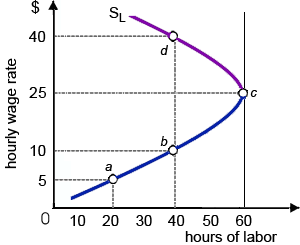

If the wage rate increases from $25 per hour to $40 per hour, in that case the elasticity of the supply of labor from this worker is roughly: (i) zero. (ii) 7/15. (iii) 13/15. (iv) one. (v) minus 13/15.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.