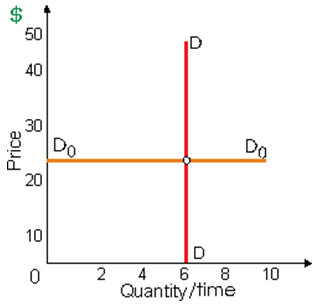

In the given figure as in below, demand curve D0D0: (w) has price elasticity of infinity. (x) is possibly for a luxury good. (y) is unitarily price elastic. (z) seems contrary to standard economic reasoning.

How can I solve my Economics problem? Please suggest me the correct answer.