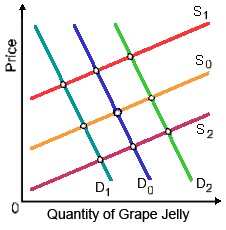

Grape jelly and Peanut butter are strong complements. Assume that severe mold ruined half of this year’s peanut harvest. When the grape jelly market was primarily in equilibrium on S0D0, then this market would shift to: (a) S1D0. (b) S0D2. (c) S2D0. (d) S2D2. (e) S0D1.

Give the right answer of the above question.