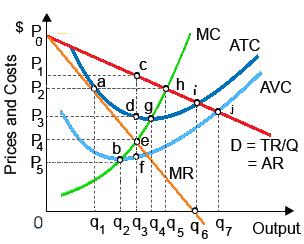

Assume that HoloIMAGine’s patents for holographic technology lapsed, as well as entry of new competitors within this market eroded the demand for HoloIMAGine technology, even though the firm retains several market power since competitors’ products are not perfect substitutes. Assume that the new demand curve facing HoloIMAGine is exactly its previous marginal revenue curve. So HoloIMAGine would be expected to as: (w) produce q2 output since minimum average variable cost corresponds to point b. (x) set its price equal to P2 and produce output Q1. (y) exit the industry because its greatest possible accounting profit is zero. (z) operate at a level of output which exceeds the efficient level for society as an entire.

Hello guys I want your advice. Please recommend some views for above Economics problems.