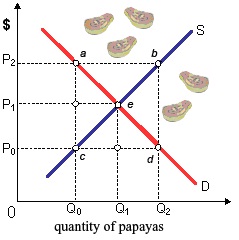

In the market of papayas: (1) A scarcity exists at P2. (2) Papayas are a free good at P0. (3) Papayas are presently a scarce good. (4) Consumer’s demand prices equivalent P2 at quantity Q2. (5) Equilibrium price for papayas be P0.

Can someone help me in getting through this problem.