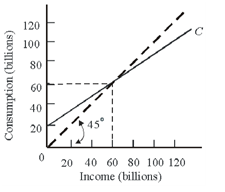

Refer to the given figure.Choose the right answer from following. If the relevant saving schedule were constructed: A) saving would be minus $20 billion at the zero level of income. B) aggregate saving would be $60 at the $60 billion level of income. C) its slope would be 1/2. D) it would slope downward and to the right