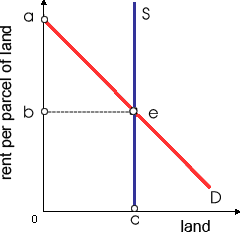

Resource of supply curve

The resource probably to conform to the supply curve demonstrated in this figure would be: (1) housing. (2) capital. (3) labor. (4) land. (5) entrepreneurship. Can someone explain/help me with best solution about problem of Economics...

The resource probably to conform to the supply curve demonstrated in this figure would be: (1) housing. (2) capital. (3) labor. (4) land. (5) entrepreneurship.

Can someone explain/help me with best solution about problem of Economics...

Refer to the below diagram, in which Qf is the full-employment output. If aggregate demand curve AD1 describes the current situation, appropriate fiscal policy would be to: A) increase taxes and reduce government spending to shift the aggregate d

Nominal interest rates are most largely and directly determined within markets for: (1) loanable funds. (2) newly issued stock. (3) foreign exchange. (4) securitized assets. (5) long term government bonds. Please c

State excess demand or inflationary gap: Excess demand takes place whenever AD is bigger than AS at the level of full employment equilibrium.

I have a problem in economics on Labor Unions-Public Employees. Please help me in the following question. Workers who are now permitted to join unions however who still might not legally strike comprise: (1) Civilian federal employees. (2) Medical pro

The elasticity of the demand for labor tends to rise as there are raises within the: (1) amount of capital utilized in a production process. (2) rate of automation in an industry. (3) difficulty in substituting between different resources. (4) share o

Can someone help me in finding out the right answer from the given options. In the year 1950 the federal government enhanced interstate highways, therefore decreasing the: (1) Demand for and the volume of highway travel. (2) Growth rate of city sprawl. (3) Demand for

I have a problem in economics on Hike in relative price of a good. Please help me in the following question. The hike in relative price of a good will quickly increase the: (i) Quantity demanded. (ii) Market supply. (iii) Rate of inflation. (iv) Quant

Can someone help me in finding out the right answer from the given options. The marginal resource cost for the monopsonist in labor market which can’t wage discriminate: (i) Is perfectly elastic. (ii) Lies above the market supply of labor. (iii) Is perfectly ine

Monsieur Cournot has a monopoly on an artesian well from that flows tasty spring water along with medicinal properties. To ignore variable costs, he is adamants that customers bring their own pails and fill them individually. Unluckil

A monopoly firm must shut down in the short run when: (w) P < minimum [average total costs [ATC]]. (x) P > minimum [average total costs [ATC]]. (y) this cannot cover all variable costs. (z) P does not equal marginal costs [MC]. Discover Q & A Leading Solution Library Avail More Than 1415862 Solved problems, classrooms assignments, textbook's solutions, for quick Downloads No hassle, Instant Access Start Discovering 18,76,764 1947975 Asked 3,689 Active Tutors 1415862 Questions Answered Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!! Submit Assignment

18,76,764

1947975 Asked

3,689

Active Tutors

1415862

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!