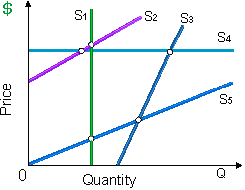

Suppose that all these illustrated curves are infinitely long straight lines. Then supply curve which is relatively (although not perfectly) price inelastic for all prices and quantities is: (1) supply curve S1. (2) supply curve S2. (3) supply curve S3. (4) supply curve S4. (5) supply curve S5.

Can someone explain/help me with best solution about problem of Economics...