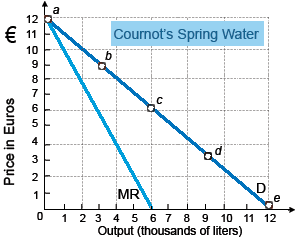

For Cournot’s Spring Water the demand is relatively price inelastic at: (i) point a. (ii) point b. (iii) point c (iv) point d. (v) point e.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.