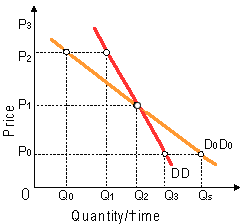

Relative to demand curve D0D0, demand curve DD: (i) is relatively more elastic than D0D0 at a price of P1. (ii) is relatively more elastic than D0D0 at a price of P2. (iii) is relatively less elastic for every quantity which would be purchased through both consumers. (iv) probably represents a good that absorbs a higher proportion of the consumer's income. (v) probably has fewer close complements than the good reflected on D0D0.

Hey friends please give your opinion for the problem of Economics that is given above.