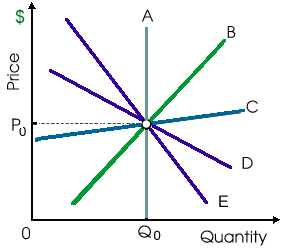

When consumer demand for this industry’s product is relatively inelastic, in that case the curve reflecting normal substitution although the least price elasticity of market demand would be of: (i) curve A. (ii) curve B. (iii) curve C. (iv) curve D. (v) curve E.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?