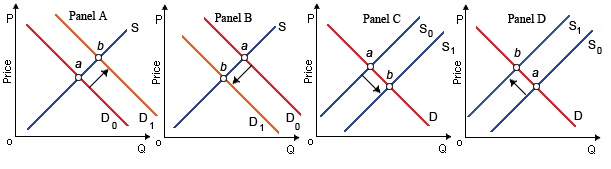

When equilibrium moves from point a to point b in the figure shown below, the only market experiencing a reduction in quantity supplied is illustrated in: (1) Panel A. (2) Panel B. (3) Panel C. (4) Panel D.

Can someone help me in getting through this problem.