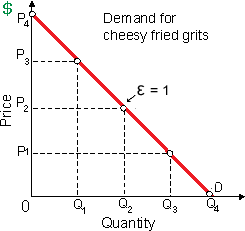

Boosting the price for Pixie’s cheesy fried grits by P2 to P3 will: (w) increases total revenue since demand within inelastic. (x) increase total revenue since demand is elastic. (y) reduce total revenue since demand is inelastic. (z) reduce total revenue since demand is elastic.

Hello guys I want your advice. Please recommend some views for above Economics problems.