Question on demand and supply

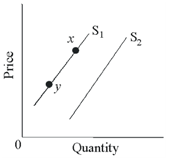

Refer to the following diagram. A decrease in supply is illustrated by a: A) move from point x to point y. B) shift from S1 to S2. C) shift from S2 to S1. D) move from point y to point x.

Technological advances have raised agricultural productivity enormously among 1800 and nowadays, and therefore, the relative incomes of family farmers declined dramatically. There hardships endured through American farm families throughout this period

Describe the implication of big number of buyers in the perfectly competetive market.

When physical capital becomes cheaper, in that case: (w) some workers may be displaced but worker productivity usually rises. (x) automation will make jobs for more workers. (y) workers will supply more labor services. (z) labor supply curves will move in backward ben

Natural barriers to entry would include: (w) long established brand loyalty. (x) enforcement of existing antitrust laws. (y) technology which dictates large plant size. (z) patents and copyright laws. Can anybody s

Define monetary policy? What monetary measure can be accepted to control the condition of excess demand? It is the policy accepted by central bank exercising control over money rate of interest and credit situatio

Choose Which one best describes the invisible-hand concept? 1) The desires of resource suppliers and producers to further their own self-interest will automatically further the public interest. 2) The nonsubstitutability of resources creates a conflict between private

When a monopolist maximizes profit and charges a price equivalent to average cost, in that case the firm: (i) is producing at the minimum point on its marginal cost curve. (ii) also charges a price equal to marginal cost. (iii) is pro

Assume that Joe discovers the price elasticity of market demand to be 0.8 for Joe’s additional fancy dehydrated water at the present price of $10 per barrel. Every barrel averages $2 to generate. Joe can: (w) increase his profits by 80% if he in

I have a problem in economics on Income and Inferior Goods problem. Please help me in the following question. For a non-vegetarian, Spam is to filet the mignon as: (1) Luxury goods are to requirements. (2) Complementary goods are to substitute goods.

Deficit budget: When expenditure of the government is greater than its receipts, it is termed as deficit budget.

18,76,764

1959840 Asked

3,689

Active Tutors

1461229

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!