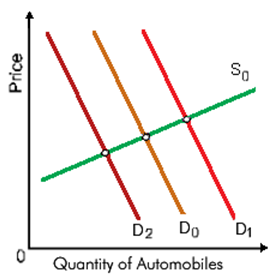

Suppose that the auto market started at the intersection of S0 and D0, and subsequently higher labor costs drove up prices for latest cars. How will it influence the market for automobiles?: (w) Higher wages for auto workers drive up the total market demand. (x) Demand shifts to D2. (y) Demand shifts to D1. (z) The quantity demanded declines back and declines up along D0.

Please choose the right answer from above...I want your suggestion for the same.