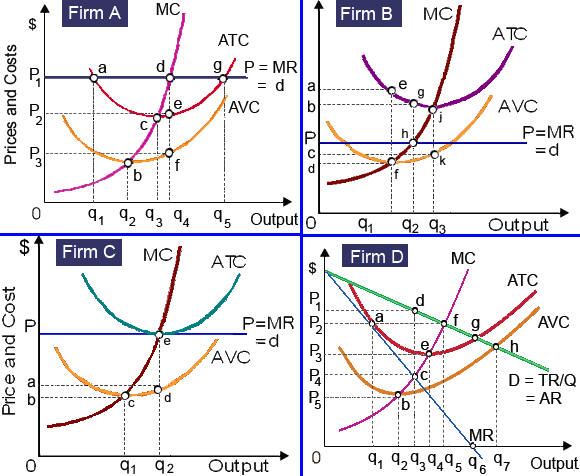

Different from Firm D, Firms A and B as well as C are all: (w) profitable firms that enjoys significant market power. (x) purely-competitive price-takers and quantity-adjusters. (y) pure monopolies. (z) perfectly inelastic suppliers.

Hello guys I want your advice. Please recommend some views for above Economics problems.