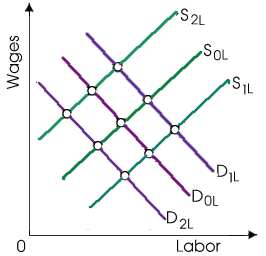

When this purely competitive labor market is firstly in equilibrium at D0L, S0L, a move to equilibrium at D1L, S0L would be inconsistent along with increases in: (w) the price of output. (x) labor productivity. (y) workers’ increased willingness to give up leisure for extra income. (z) the numbers of firms in industries hiring labor through this market.

Hey friends please give your opinion for the problem of Economics that is given above.