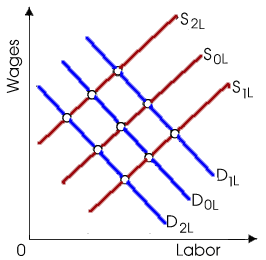

When this purely competitive labor market is firstly in equilibrium at D0L, S0L, an increase within the price of output will result into equilibrium being attained at: (w) D0L, S0L. (x) D1L, S1L. (y) D2L, S1L. (z) D1L, S0L.

Hello guys I want your advice. Please recommend some views for above Economics problems.