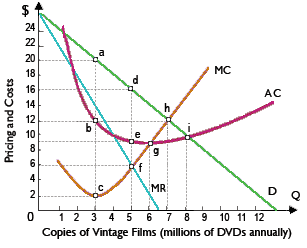

The profit-maximizing price for “Silver Screen Classic” of Nostalgia DVDs is: (i) $6 per copy. (ii) $10 per copy. (iii) $12 per copy. (iv) $16 per copy. (v) $20 per copy.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.