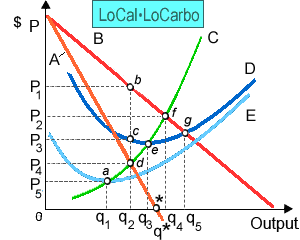

When LoCalLoCarbo, the favorite corporation of fad dieters, produces adequate output to minimize its average total costs that will: (1) produce more than the profit-maximizing level of output. (2) concurrently minimize its average variable cost. (3) precisely break even since its total revenue will equal its total costs. (4) receive a normal rate of return on its investment. (5) concurrently maximize its economic profit.

How can I solve my Economics problem? Please suggest me the correct answer.