Production possibilities analysis

Refer to the given diagram. As it associate to production possibilities analysis, the law of increasing opportunity cost is reflected in curve:1) A 2) B 3) C 4) D Help me to answer above question

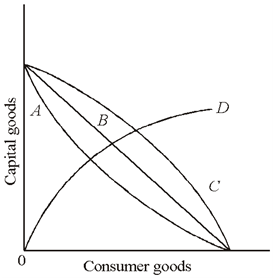

Refer to the given diagram. As it associate to production possibilities analysis, the law of increasing opportunity cost is reflected in curve:1) A 2) B 3) C 4) D

Help me to answer above question

The marginal tax rate upon earned income under negative income tax system demonstrated in this figure is: (1) 15 percent. (2) 20 percent. (3) 25 percent. (4) 33.3 percent. (5) 50 percent. Q : Weakest and least efficient producers Cartels are generally supported most strongly by: (w) the largest and most efficient producers in the industry. (x) the weakest and least efficient producers in the industry. (y) buyers of the output of the industry. (z) consumer advocate groups.

Cartels are generally supported most strongly by: (w) the largest and most efficient producers in the industry. (x) the weakest and least efficient producers in the industry. (y) buyers of the output of the industry. (z) consumer advocate groups.

Each and every profit-maximizing firm which can cover its variable costs will hire the labor: (1) Just to the point of the diminishing returns. (2) Just to the point where MRP = ARP for the final worker hired. (3) Beyond the point of the diminishing r

Tell me the answer of this question. Economists would describe the U.S. automobile industry as: A) purely competitive. B) an oligopoly. C) monopolistically competitive. D) a pure monopoly.

Unlike a purely competitive firm, a monopolist can: (w) select a price and sell as much as this needs (x) equate marginal revenue as well as marginal cost to maximize profits. (y) produce any required amount and sell as much as this d

I have a problem in economics on Problem on falling income causes increase in demand. Please help me in the following question. If falling income causes the demand for a good to rise, it is an: (1) Inferior good. (2) Costly biological necessity. (3) N

I have a problem in economics on Subjective preferences of Marginal Utility. Please help me in the following question. The Marginal utilities: (1) Reflect the subjective preferences. (2) Are realistically evaluated by wealth. (iii) Are set by the demo

Government tax revenue would raise most from a specified tax when the good taxed contain a relatively: (w) price elastic demand. (x) price inelastic demand. (y) unitary price elastic demand. (z) flatter demand curve. Q : Monopsonistic Exploitation and Wage Can someone please help me in finding out the accurate answer from the following question. If a firm's wage structure reflects the keenness of individual employees to work, terms which are most applicable comprise: (i) Monopsonistic exploitation and the wage discrimin

Can someone please help me in finding out the accurate answer from the following question. If a firm's wage structure reflects the keenness of individual employees to work, terms which are most applicable comprise: (i) Monopsonistic exploitation and the wage discrimin

The arbitrager is an organization or individual that will: (1) Simultaneously purchase low and sell high in various markets. (2) Create disparities among prices in various markets. (3) Resolve disputes among sellers and consumers. (4) Purchase low and

18,76,764

1936400 Asked

3,689

Active Tutors

1437953

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!