Problem regarding market demand curve

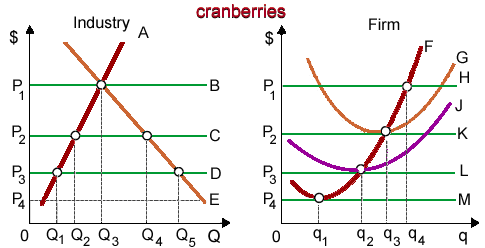

Hey friends I need your help for illustrated figure in below where for cranberries, the market demand curve is: (i) A. (ii) B. (iii) F. (iv) J. (v) E. Please give your suggestion for this problem…

Hey friends I need your help for illustrated figure in below where for cranberries, the market demand curve is: (i) A. (ii) B. (iii) F. (iv) J. (v) E.

Please give your suggestion for this problem…

For any profit-maximizing monopolist not capable to price discriminate, production arises at an output level where is: (w) price exceeds marginal costs [P > MC]. (x) marginal revenue exceeds marginal costs [MR >

The revenue added through selling an additional unit of output is: (w) demand elasticity. (x) average profit rate. (y) supply elasticity. (z) marginal revenue. How can I solve my Economics problem?

An increase in consumer desire for strawberries is most likely to: increase the number of strawberry pickers needed by farmers. reduce the supply of strawberries. reduce the number of people willing to pick strawberries. reduce the need for strawberry pickers

Suppose a doctor has a private clinic in New Delhi and his annual earnings are of Rs10 lakh. When he works in a Government Hospital in New Delhi, his annual earnings are of Rs 8 lakh. Determine the opportunity cost of encompassing a clinic in New Delhi?

Break-even levels of output for a firm happen where is: (w) total revenue equals total economic cost. (x) accounting profits are zero. (y) total variable cost equals total fixed costs. (z) competitive firms will shut down within the short run.

A firm along with market power faces a downward sloping demand curve since: (w) selling more of the good needs a price cut. (x) marginal revenue should equal average revenue. (y) only pure monopolies face horizontal demand curves. (z)

Setting a minimum price floor above the equilibrium price will: (w) raise the equilibrium price. (x) create excess demand at the minimum price. (y) create excess supply at the minimum price. (z) clear the market at the minimum price.<

Line T0 depicts a tax system which is: (1) progressive. (2) recessive. (3) proportional. (4) biased. (5) regressive. Q : In the quintile distribution of income In the quintile distribution of income, the term "quintile" represents

In the quintile distribution of income, the term "quintile" represents

Revenue: This refers to total money income from the sale of output.

18,76,764

1936201 Asked

3,689

Active Tutors

1428876

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!