Problem on tax system

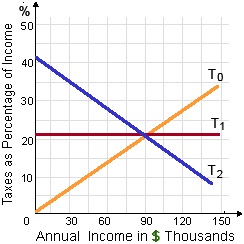

In the figure shown below, line T0 depicts a tax system which is: (1) Progressive. (2) Regressive. (3) Proportional. (4) Unbiased. (5) Recessive. Please someone suggest me the right answer.

In the figure shown below, line T0 depicts a tax system which is: (1) Progressive. (2) Regressive. (3) Proportional. (4) Unbiased. (5) Recessive.

Please someone suggest me the right answer.

What is the base of categorizing receipts into revenue and capital receipts?

For every value of real GDP, actual investment equals? A. Planned Investments B. The difference between planned investments and actual saving. C. The difference between planned saving and actual saving. D. Planned Saving

What points out revenue deficit? Answer: Revenue deficits are stated as the surplus of revenue receipts. Revenue Deficit = Revenue Expenditure - Revenue Recei

Gross domestic capital formation is always greater than gross fixed capital formation

Between 1961 and 2007, the rising share of the Canadian population in paid employment contributed to rising GDP per person. But suppose that the share of the Canadian population in paid employment had remained constant between 1961 and 2007. What would Canadian GDP pe

Describe why businessmen mostly wish to open current account in bank?

When equilibrium moves from point a to point b in the figure shown below, the only market experiencing a rise in demand is illustrated in: (1) Panel A. (2) Panel B. (3) Panel C. (4) Panel D. Q : Full-employment Define the " Define the "full-employment" or "natural" rate of unemployment and give its approximate percentage rate as economists currently define it.

Define the "full-employment" or "natural" rate of unemployment and give its approximate percentage rate as economists currently define it.

Meaning of Fiscal policy:Fiscal policy is the set of decisions and principles of a government regarding the extent of public expenses and mode of financing them. It is about the attempt of g

Can someone help me in finding out the right answer from the given options. The consumer maximizes utility whenever the spending patterns cause: (1) Marginal utility of each and every good to be at its maximum value. (2) Marginal utilities of each and every goods cons

18,76,764

1931508 Asked

3,689

Active Tutors

1428043

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!