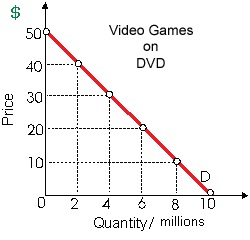

The demand curve for DVD games is a straight line, therefore its slope: (1) Is constant, although price elasticity of demand drops/falls as output increases. (2) Price elasticity are both stable. (3) Is constant, although price elasticity of demand increases as the price drops/falls. (4) Differs to compensate for modifications in elasticity.

Can someone help me in getting through this problem.