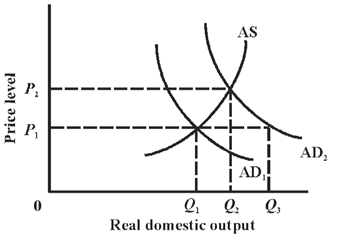

Problem on price level-real domestic output

Refer to the below diagram. Give me answer of this question. If equilibrium real output is Q2, then: A) aggregate demand is AD1. B) the equilibrium price level is P1. C) producers will supply output level Q1. D) the equilibrium price level is P2.

A Lorenz curve is a way to demonstrate: (w) that the U.S. has perfect equality of income distribution. (x) a mirror image of a production-possibility curve. (y) the percentages of families receiving different percentages of income. (z) differences wit

Choose the right answer from following. Tariffs: A) may be imposed either to raise revenue (revenue tariffs) or to shield domestic producers from foreign competition (protective tariffs). B) are also called import quotas. C) are excise taxes on goods exported abroad.

I have a problem in economics on History of Industrial Unions. Please help me in the following question. Industrial unions historically tried to systematize all the workers in: (i) A Specific Company or broad industry. (ii) The United States. (iii) A specific craft or

The automakers slashed prices and gave ‘zero percent financing’ throughout the year 2001-2003 recession. An expected outcome was: (1) The decline in the demand for utilized cars. (2) enhanced maintenance of older cars by their owners. (3) Buyers purchasing

Grape jelly and Peanut butter are strong complements. Assume that severe mold ruined half of this year’s peanut harvest. When the grape jelly market was primarily in equilibrium on S0D0, then this market would shift to: (a) S1D0. (b) S0D2. (c) S2D0. (d) S2D2. (e

The present value of an annual income stream which goes onto forever is: (w) infinite. (x) zero. (y) the annual income multiplied through the interest rate. (z) the annual income divided through the interest rate.

The competitive workings of the market for soy beans would be distorted when: (1) Europe experiences a severe drought and has paltry harvests this year. (2) Ethiopia imports soy beans to feed its hungry masses. (3) the U.S. imposes a soy bean embargo forbidding export

I have a problem in economics on Quantity demanded vary inversely. Please help me in the following question. The law of demand defines that price and: (1) Quantity demanded differ directly. (2) Quantity demanded differs inversely. (3) Demand differs d

Competitive firms determine this difficult to exploit consumers as: (w) consumer boycotts generate bad publicity. (x) market distributions of products are uniformly fair. (y) government price ceilings equivalent opportunity costs. (z) prices that exceed costs attract

Sticky prices within oligopoly markets are: (w) predicted by the kinked demand curve model. (x) substantiated by many statistical studies. (y) most common for highly differentiated products. (z) a result of price discrimination. Discover Q & A Leading Solution Library Avail More Than 1438753 Solved problems, classrooms assignments, textbook's solutions, for quick Downloads No hassle, Instant Access Start Discovering 18,76,764 1951888 Asked 3,689 Active Tutors 1438753 Questions Answered Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!! Submit Assignment

18,76,764

1951888 Asked

3,689

Active Tutors

1438753

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!